How digital is client onboarding in the Austrian financial sector?

Next-Generation Client Onboarding

Digital client onboarding is now firmly established in the Austrian financial sector

Platform providers such as MyTaxi, Uber or AirBnB have set new benchmarks for innovative, lean onboarding solutions that customers now also expect from their bank.

“The possibility to open an account and select products online is an important success factor in digital onboarding. Through seamless, digital-only client onboarding the main banking groups in Austria have reduced the time required to open an account to less than 10 minutes. Furthermore, it enables instant account activation."

Direct banks and private banks are leading the way

Most banks now offer basic products and additional services online. You rarely need to visit your branch, and then only for products requiring specialist advice. Direct banks and private banks are leading the way in digital onboarding whilst the major banks are lagging well behind. Cooperative banks, saving banks and car finance companies rank towards the middle of the table.

Digital presence as opportunity

Today’s customers are quicker to switch if their current bank does not meet their wishes. Unsatisfied customers cancel the registration process and go for a competitor’s product. The customer experience thus has a significant impact on closure rates.

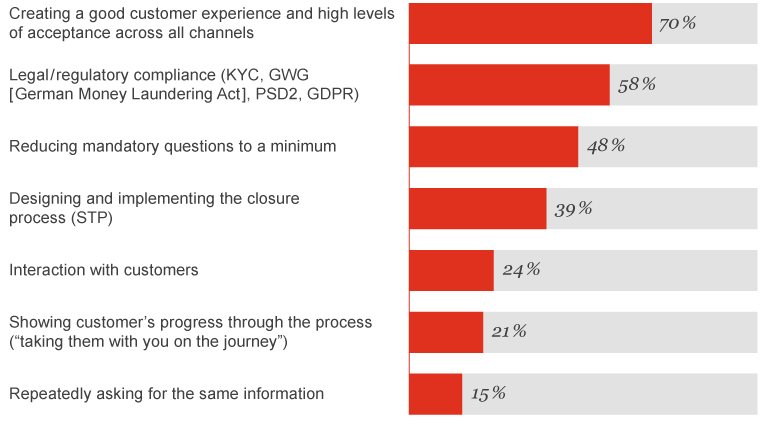

Top currrent challenges in client onboarding

The next stage: merging of all customer interaction channels

Leading digital financial institutions are gradually developing their onboarding into a multichannel process that is accessible from all devices. The industry is now entering the next stage: next generation client onboarding.

This will focus mainly on digital customer experience and merging of all customer interaction channels to a single channel. Digital transformation often fails due to legacy organisational structures or restrictive IT systems. Current transformation projects demonstrate that financial institutions are rethinking to counter the growing pressure from competition as well as rising customer expectations.

Future trends:

Products and services: Consumers expect to be able to obtain financial products and services digitally. Cooperative banks, private banks and direct banks have the largest digital product and service offering. Current accounts, instant access accounts, consumer finance, credit card and deposit accounts are the most frequent online products.

Digital client experience: Three quarters of the institutions surveyed offer seamless onboarding from a PC or mobile device. However, they have not yet established advanced digital assistance systems such as text-to-speech or chatbots.

Digital distribution channels: Analyses of digital contact points with the customer provide detailed real-time information on how users interact with the web application to help identify obstacles along the customer journey at an early stage. These distribution-channel analyses are well established in most financial institutions.

Data landscape: Legacy structures mean that there are a number of different systems in operational use. Half of the financial institutions surveyed purchase personal data from third-party providers. These serve inhouse business processes to comply with legal requirements or for the strategic planning of marketing and sales tasks.

Customer identification process: The customer identification process differs widely across banks. Banks with branches identify customers in the branch directly, via traditional mail, through €1 transfer or via video call. Online banks rely mainly on photo identification. Both, traditional and online banks perform automated checks, like KYC, in the background.

System and process requirements: Complex transaction systems, back-office processing and specialised web applications are the final part of the client onboarding process and need to meet the highest industry standards. In addition, strict legal and regulatory requirements represent a constant challenge for IT and business processes. At the same time, new regulations create new market conditions and promote the liberalisation of the market. For example, the Payment Services Directive II (PSD 2) made it easier for payment, robo-advice or PFM service providers to enter the financial sector and provide access to the banking infrastructure.

Conclusion: Overall, the digitisation degree and customer experience of traditional banking firms in Austria approach the onboarding model of online banks.

Contact us

Enzo Orsi

Partner, Head of Financial Services Technology Consulting, PwC Austria

Tel: +43 699 163 052 09

Paramvir Parhar

Core Banking and Customer Journeys Leader, PwC Austria

Tel: +43 699 163 05 445